Everyone deserves an opportunity to invest in precious metals; it’s a value that we hold true and will never ignore, and we make sure that this is clear from the get-go.

We have organized every single piece of information you may need to know into separate, digestible 2-4 page sections, as illustrated in our table of contents. No matter the question you have, you can find it by navigating through this page.

Request Our Free Investment Guide

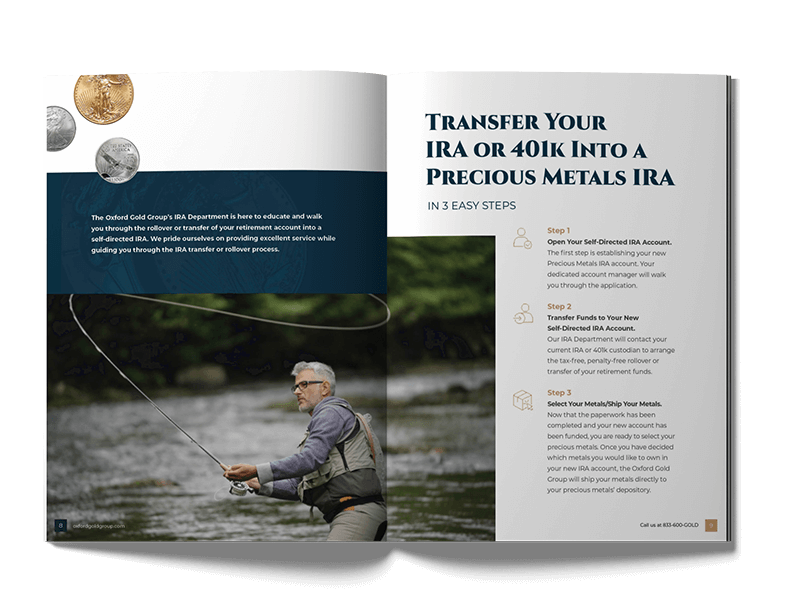

One of the most uncertain parts of creating a Precious Metals IRA is figuring out how to transfer your current IRA’s funds into the new one.

We make this process much more straightforward than you’d believe, so much so that it can be outlined in just three steps, as seen on the page. As is with the rest of the guide, we make sure that understanding this process is easy for you so you can get straight to investing.

Request Our Free Investment Guide

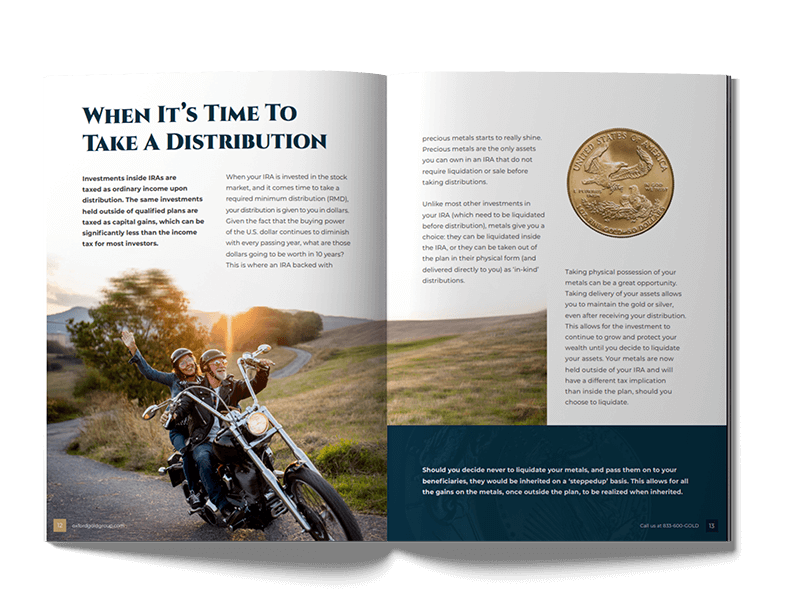

One of the many benefits of a precious metals IRA starts to shine whenever it’s time for you to take your first required distribution.

Unlike with a normal IRA, you can pull out precious metals in their physical form (rather than having them liquidated) so that your investment can continue to grow in value. Although this is great, there are even more benefits to a precious metal IRA that you can learn about.

Request Our Free Investment Guide

After reading through our entire guide, you’ll likely be ready to make your decision on whether or not to start investing, and Oxford Gold Group has you covered.

We’re always ready to help you in any regard, whether it's placing a new order, creating an account, or anything else involved in the process that we clearly outline in this guide. Don’t hesitate to start learning today and download our guide now to learn how you can secure your future.

Request Our Free Investment Guide